Retirement plan options for small business owners and self-employed individuals explained

Deciding on what path to take to maximize retirement savings can be tricky, especially when faced with so many options that contain small differences. With each day that passes, there is less time to build a fund that would suffice a comfortable life after retirement. There are many different reasons to consider a specific plan, including what level of financial security you want to enjoy, retirement goals, long-term healthcare needs, tax liabilities and more. Here at The Hechtman Group, we have the industry experience to inform and guide you through planning for your retirement.

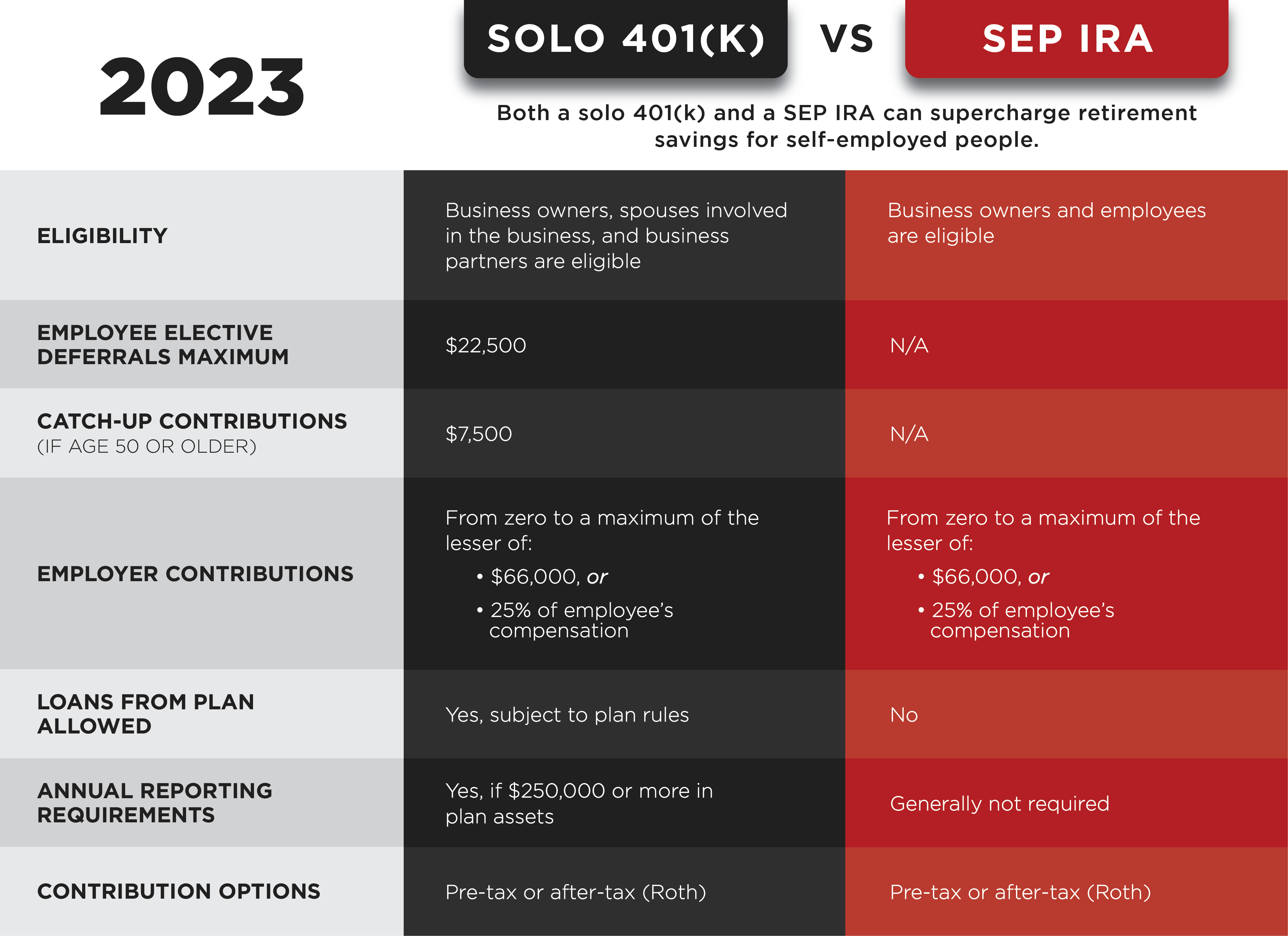

What are SEPs and Solo 401(k) plans?

SEPs and Solo 401(k) plans are both retirement savings plans designed specifically with small business owners and self-employed individuals in mind. There are a few nuanced differences between these plans within their flexibility, contribution limits, and eligibility.

What is the difference between these plans?

The first difference between an SEP and a Solo 401(k) retirement plan is that Solo 401(k) plans generally allow greater flexibility in regard to contributions. First and foremost, they allow for larger contribution limits. For example, in 2023, the maximum contribution limit for a Solo 401(k) plan is $66,000, and $73,500 if you are over 50 years old. $22,500 of the Solo 401(k) limit comes from the employee compensation and 25% is the employer match. Alternatively, the maximum contribution limit for an SEP is the lesser option of $66,000 or 25% of compensation. Secondly, Solo 401(k) plans allow contributions from both employers and employees, whereas SEPs only permit employers to make contributions.

SEP plans also require all contributions to retirement plans by the employer to be equal, whereas Solo 401(k) plans do not. This can be a disadvantage to those looking to invest more into their own retirement as opposed to their employees.

The next difference between these plans lies within its requirements for eligibility. Only businesses with no full-time employees besides the owner and their spouse can enroll in a Solo 401(k) plan. An SEP plan can be offered to select part-time employees contingent on them meeting certain criteria.

Which one should you choose?

Depending on the infrastructure of your business, there are several retirement options built around strengthening your savings. SEP and Solo 401(k) plans are most ideal for small business owners and self-employed individuals. Selecting the right retirement plan of the two depends on specific criteria that your business may or may not meet, such as whether you staff full-time employees or not.

To learn more about which plan fits your business the best, contact us today. Upon first contact, we will begin strategizing a retirement method that is in line with the characteristics of your business, individual lifestyle habits, and retirement goals. The Hechtman Group goes the extra mile to ensure we understand your business from top to bottom before recommending the best course of action.

At The Hechtman Group Ltd, we understand that tax laws and regulatory and IRS requirements for real estate are vastly different from other financial services. Rich in industry experience, our CPAs and accountants can guide you through all the necessary steps while also creating best practice opportunities for long-term growth.

Our services include expertise in financial reporting, disposition planning, acquisition analysis, energy credits and deductions, tax planning and more.